Planning for retirement just got a significant boost with the updated IRS contribution limits and key provisions from the SECURE Act 2.0. For 2025, indiveduals can enjoy higher contribution limits, new catch-up opportunities, and expanded options like Roth conversions and 529 rollovers. These changes not only help savers maximize their retirement funds but also introduce new flexibility for managing savings. Here’s a breakdown of the updates and strategies to help you stay ahead in your financial planning journey.

2025 IRA Contribution Limits: Simplified and Enhanced

Higher Contribution Limits

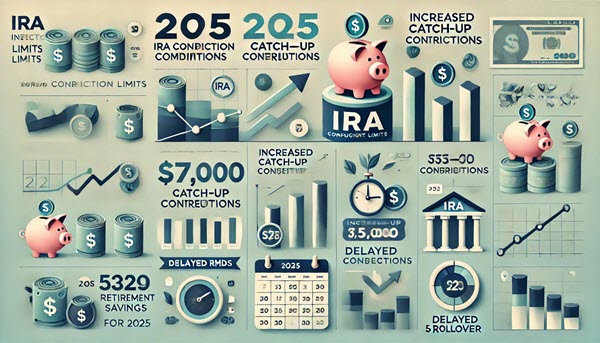

- For 2025, the annual IRA contribution limit has been raised to $7,000.

- Individuals aged 50 or older can contribute an additional $1,000 catch-up amount, offering an opportunity for older workers to bolster their retirement savings as they near retirement.

The Role of Inflation Adjustments

- Inflation adjustments are a critical factor in determining annual IRA contribution limits. These periodic increases ensure that savings potential keeps pace with rising living costs.

SECURE Act 2.0: Key IRA Updates for 2025

The SECURE Act 2.0, enacted in late 2022, has reshaped retirement savings rules, with significant implications for Individual Retirement Accounts (IRAs). Here’s a streamlined overview of the most important updates for 2025 and beyond:

1. Increased Catch-Up Contributions

- Higher Limits for Ages 60-63: Starting in 2025, individuals aged 60 to 63 can make enhanced catch-up contributions to their retirement accounts. For IRAs, this could mean exceeding the standard $1,000 catch-up limit available to those aged 50+.

- Why It Matters: This change is especially beneficial for those nearing retirement who aim to maximize savings during their peak earning years.

2. Roth IRA Catch-Up Contributions

- Income-Based Rules: From 2024 onward, individuals earning more than $145,000 (indexed for inflation) must allocate all catch-up contributions to a Roth account. Contributions to Roth accounts are made after-tax.

- Strategic Implications: While this primarily affects employer-sponsored plans, IRA savers considering Roth conversions should take this into account for long-term planning.

3. Auto-Enrollment and Rollover Opportunities

- Auto-Enrollment Influence: The SECURE Act 2.0 promotes auto-enrollment in employer retirement plans, encouraging consistent savings and potentially reshaping individual IRA contributions.

- 529 Rollovers to Roth IRAs: Individuals can roll over unused funds from 529 college savings plans into Roth IRAs, with a lifetime cap of $35,000. This offers a flexible way to repurpose education savings for retirement.

4. Delayed Required Minimum Distributions (RMDs)

- The RMD age increased to 73 in 2023 and will rise to 75 by 2033.

- Opportunities: This delay allows for extended tax-deferred growth and provides a window for strategic Roth IRA conversions, reducing future taxable income.

5. Emergency Withdrawals and Savings Incentives

- Emergency Access: Beginning in 2024, individuals can withdraw up to $1,000 annually penalty-free from a retirement account for emergencies. This feature reduces hesitation to contribute due to fears of limited access to funds.

- Saver’s Match Program: The federal government now matches contributions for qualifying low- and moderate-income earners, incentivizing IRA contributions and boosting savings.

6. Student Loan Repayment Matching

- Employers can now match student loan repayments with contributions to retirement plans. While this primarily affects employer-sponsored plans, it indirectly benefits IRA savers by reducing the need to choose between debt repayment and retirement contributions.

7. Roth IRA Opportunities for Employer Rollovers

- Expanded provisions allow easier rollovers from employer-sponsored Roth plans to Roth IRAs, streamlining account management and optimizing tax benefits for retirees or job changers.

8. IRA Contributions for Non-Traditional Income

- The Act now permits IRA contributions from non-traditional income sources, such as stipends and fellowship payments, empowering graduate students and postdoctoral fellows to start saving earlier.

What Does This Mean for You?

The updates introduced by the SECURE Act 2.0 present both challenges and opportunities. For 2025, consider these steps to optimize your retirement strategy:

- Maximize Contributions: Take full advantage of increased limits and catch-up opportunities.

- Plan for Roth Conversions: Use low-income years to shift funds into Roth accounts before RMDs begin.

- Incorporate New Rules: Factor in the Saver’s Match, emergency withdrawal options, and auto-enrollment influences.

- Reassess Long-Term Goals: Explore strategies for extended tax-deferred growth, streamlined account management, and maximizing incentives under the updated regulations.

By staying proactive and informed, you can make the most of these changes and secure a more robust retirement future.